Although it's not possible to get out of this quagmire, at the very least, it can be ameliorated by dumping the euro for the peseta. It's no surprise then that calls for the secession of Catalonia are gaining strength. Of course, anecdotes of a few Spanish companies emerging stronger during the crisis exist, but a few triumphant companies do not an economy make.

Anyway, you should read this fascinating op-ed piece titled Banks should learn from Habsburg Spain, because it also touches on money, an issue which we will elaborate further in this post. In this op-ed piece, the two academicians—both economic historians—explain how 16th century Habsburg Spain got away with debt restructuring, not once but four times:

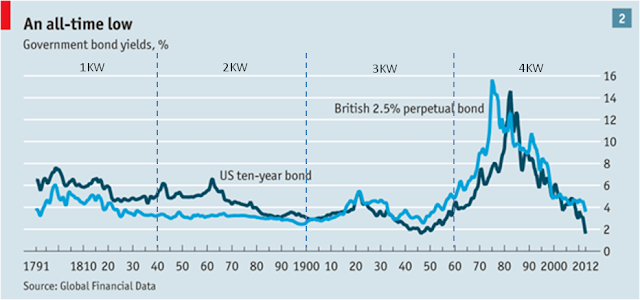

Investors in the volatile debt of Ireland, Portugal, Spain and Italy can be forgiven a sense of déjà vu. The history of sovereign debt is strewn with promises broken, creditors losing their shirts (and sometimes literally their heads) and, during defaults, economic malaise. So does the long, melancholy history of government borrowing offer any lessons for policy makers today?The above op-ed piece doesn't tell the full story. To understand the background to 16th century Spain's predicament, we have to go back to the Christian reconquest of Spain which was consummated in 1492, thanks to the cannon, without which the Moors would have been secure in their fortress-town. Actually, the process took a long time as the Moors had been generally defeated by 1249 and from thereon, had been confined to the southern region of the Iberian peninsula. It must be noted that the Inquisition that was associated with the reconquest led to the expulsion of Jews and Muslims, a major economic loss to Spain. The Jews were traders and also bankers, without whom credit would disappear.

Carmen Reinhart and Kenneth Rogoff, in their classic study of eight centuries of financial crises, argue that the repeated folly of investors is the cause of sovereign debt problems. After a few good years, creditors forget the risks, lend recklessly, then end up snared in a default. The cycle soon restarts as new investors convince themselves “this time is different”.

At the dawn of sovereign lending, King Philip II of Spain – ruler between 1556 and 1598 of the only superpower of his age – signed hundreds of loan contracts. He also became the first serial defaulter, halting payments four times. The story of a powerful monarch able to convince creditors to lend as much as 60 per cent of gross domestic product while defaulting again and again offers useful insights into how the bargain can be improved.

Sovereign debt crises today “hurt” in three ways. First, when bond markets panic and yields rise in a downturn, taxes are raised and spending is cut. Austerity aggravates the slump. Second, a country’s banking system typically implodes. Third, the return to debt markets is often long delayed; state employees are sacked, contractors go unpaid, and the economic slump deepens.

By contrast, Genoese lenders to Philip II created a safe and stable sovereign borrowing system. It survived shocks such as the failed 1588 invasion of England with the Armada. Most bankers lent to the king for decades; no lender lost money in the long term. Financiers simply charged higher rates in normal times to compensate for the risks during crises.

When shocks hit – such as a combination of low silver revenues and a costly war against the Ottomans – debt contracts were not expected to be honoured to the letter. Renegotiations were concluded fast – in 12 to 18 months, compared with today’s average of six to seven years. “Haircuts” for investors, from 20 to 40 per cent, were moderate. Lending resumed promptly.

Even in normal times, lenders and borrowers shared risk effectively. A large fraction of Philip II’s short-term debt was “state contingent” – repayment terms and interest rates were automatically adjusted in line with fiscal conditions. In bad times – when the silver fleet from the Americas was small, say – the king either repaid less or extended the maturity of a loan. This avoided the need to let soldiers go unpaid.

Automatic loan modification enabled Spain to avoid negative feedback loops such as those seen in southern Europe today, with falling tax revenue leading to austerity and hence an even more severe slump. The ability to write state-contingent debt using an easily observed indicator of fiscal health, such as the arrival of a fleet, was crucial. In modern debt markets, verifiable indicators such as value added tax receipts, certified economic growth figures or world oil prices could be used as measures of fiscal strength.

The practices of the bankers, too, offer lessons for today. Loans were expensive and profits high. The Genoese absorbed losses easily because of their low leverage. Instead of borrowing themselves or taking deposits (as earlier competitors had done), they mostly financed themselves with equity. In addition, they sold the lion’s share of each loan on to other investors. Profits and losses were then distributed proportionately. During crises, everyone suffered, but no toxic concentration of risk threatened the bankers’ survival. In other words, risk transfers that failed during the recent subprime crisis worked well in the 16th century.

Repeated cycles of lending and default, contrary to common belief, are not a sign of bankers’ stupidity. Often, creditors have realised that “next time will be the same”, and prepared themselves accordingly. They have provided effective insurance to the sovereign, and absorbed losses with thick equity cushions. The age of the galleon produced effective risk-sharing and a stable banking system; the age of the internet and jet travel is failing to do the same.

Credit is money, more important than gold or silver. However credit can't exist on its own without the productive capacity of the land and its people. Without any produce, there's no way to repay the credit extended. Credit facilitates production and trading of the produce. Credit provision is a skilled profession since it entails convincing depositors to place their excess money with the credit providers while on the other side, the credit providers must be exceptional in assessing the risk of borrowers. This calls for a knowledge of the borrowers' characters and their income producing capabilities. The credit providers must also be part of a network of similar credit providers so that, aside from better information gathering and sharing, one can make up for a temporary shortfall in funding by temporarily borrowing from others. Simply put, the things that stand a lender in good stead are a strong reputation, good intelligence gathering and being part of a network. That's why you can't easily replace them. Modern big banks are weak in one crucial aspect: poor knowledge of the borrowers' characters. Worse still, the securitisation of debts which is intended to drive down the cost of money paradoxically severs the relationships between lenders and borrowers, making the debts costlier when borrowers eventually default.

As for the Moors, they were not only good agriculturalists but were also strong in science and mathematics. They introduced irrigation systems alongside new food crops, such as sugar, cotton, lemons, oranges, hard wheat and rice. In industrial production, they established paper making, steel, silk and leather industries. Once the people involved in these industries were gone, the locals could not easily take over as more critical than the physical availability of land, machines and labour were the organisational abilities of the people running the industries. It must be remembered that in Spain then, only 10% of the land was suitable for grain farming because most of the land lay in the dry region.

The northern Christian Spaniards were skilled in raising sheep. One of the reasons for their interest in conquering the Moorish territory was to enable them to take their flocks south for winter pasture. But sheep grazing ruined the agricultural land that the Moors had cultivated. It so happened also that the extended cold periods known as the Little Ice Age had descended in 1315 and it was to last until 1720. As winters became harsher and summers cooled, large areas of fertile land were no longer viable for farming. It is therefore not surprising that the Inquisition occurred during these times as Spain had been hard hit economically, a combined result of their leaders' short-sightedness and adverse weather phenomena. Famine and plague were a feature not only of Spain but also Europe in the 14th and 15th centuries.

To escape this destitute, Spain was forced to find wealth elsewhere. This was the trigger for the voyage of Christopher Columbus, part-financed by the Spanish monarchy with the other half by private Italian investors. Columbus's primary goal was not spices but precious metals, especially gold as Spain was badly short of money. Columbus only found a limited loot of gold but he paved the way for subsequent conquistadors, operating as private enterprises, to subdue the Aztec and Inca empires. Both the Aztec and Inca empires had caches of gold mined over thousands of years. But of far greater consequence was their silver mines which were the main sources of economic wealth for Spain. Those two empires were easy pickings because their societies had been hierarchically organised; by decapitating the heads, resistance easily crumbled. Still, the conquistadors needed the assistance of the smallpox virus to finally vanquish both empires.

In total, approximately 180 tons of gold and 16,000 tons of silver reached Spain. Gold supply peaked around the 1550s while silver around the 1600s. Silver supply declined by 1630 and by 1640, Spain was on the brink of collapse. But how did Spain use the wealth from its colonies? Although Spain had wealth, it didn't have money because its credit mechanism had ceased to function or had become expensive with the flight of its Jewish bankers. Nonetheless, it must get the wealth flowing to its people, that is, those who didn't become conquistadors in its colonies, in order to preempt social troubles at home. Historically, there are two ways of achieving this: you can either build grand buildings, in the manner of Ancient Rome, so that the jobless get employed or you can pack them off to wage wars on foreign soil, exporting discontent to ensure peace at home. As related in the above op-ed piece, it's the latter option that was chosen by Charles I, the first King of Spain (1516-1556), also known as Charles V, Holy Roman Emperor (1519-1556). Keen to project power abroad, he fought with an alliance of France and the Ottoman empire and his battles were generally successful.

Wars require massive financing and for 16th century Spain, this meant access to credit. The bullion shipments from the Americas did not arrive in a constant stream. Some were waylaid by privateers or sank to the bottom in bad weather. Only credit could make up for these misfortunes. Since credit was not available in Spain, Charles I had to borrow from abroad, initially from the the Fuggers of Bavaria. After a string of defaults which temporarily bankrupted the Fuggers, Spain turned to the Genoese for financing.

When Charles I abdicated, his son, Phillip II (1556-1598), inherited not only the crown but also his father's debt of 36 million ducats. This did not prevent him from ruinously expanding the war against England, the Netherlands and the uprising Protestants in the German lands. The bullion was one thing but it was the credit expansion that actually fuelled the war and gave rise to the inflationary 150-year Price Revolution from the beginning of the 16th century to the first half of the 17th century. Without credit, it's not easy to spend physical silver coins.

Also, more important, was Spain's inferior economy relative to that of other European countries. Just imagine if the Spanish empire had been a commercial one, like the Dutch or British, all the bullion flowing to Spain would have been stored in its vault. The economic activities in Europe would have suffered as Spain would have been an economic winner, sucking all wealth from both its colonies and Europe. Instead as an economic loser, it had to distribute its bullion to the winners, namely the Dutch, Italians, French, English and Germans. But that loser kept on receiving wealth and only a major war ensured that that wealth was immediately spent.

The reason why the Genoese bankers continued to extend credit to Spain despite four debt restructuring was because the bankers knew that silver from the Americas would keep on flowing and, equally important, they had Spain by the balls the moment Spain became bogged down with warfare. Moreover, the Spanish sovereign debt was a case of monopsony - many sellers but only one buyer. So it was easy to share the debts among many lenders as all lenders knew who the borrower was.

Therefore, given those conditions, the lessons from the above debt restructuring cannot be applied to the current Euro crisis because aside from Germany, most of the Euro countries aren't competitive because of the expensive Euro. They are able to survive for now, thanks to the financial assistance extended by the EU but that will soon end and those troubled countries will lurch back into an even worse crisis given their worsening debt situation.